October 28, 2020

SLAWS Update

The Committee for Employment & Social Security’s (ESS) report on Supported Living and Ageing Well Strategy (SLAWS) : Extending the Life of the Long-term Care Insurance Scheme was debated in August 2020. Whilst this is old news there will be significant challenges for the new States to tackle as a result of the decisions made in August and therefore it is worth reviewing what the States decided. In August 2020 the States agreed:

1. payments for a care home beds, were not enough to ensure that there would be investment in the future to meet the demand

2. to increase the rates paid to care homes with the required changes to legislation, budgeted costs, and potential future rises in contributions

3. to increase how much individual residents would pay over the next 2 years as well as this year

4. to agree that the benefits would be reviewed every 5 years and that interim reviews could be conducted, if ESS thought there was significant pressure on the cost of delivering long-term care

5. to agree to introduce a higher rate of benefit for exceptional and complex cases

6. to develop suitable eligibility and assessment criteria for access to the benefit in 5. above no later than December 2020

7. to agree, in principle, that the Long-term Care Scheme should be extended to cover care provided at home and to direct ESS and the Committee for Health & Social Care (HSC) to develop detailed implementation plans for this proposal no later than June 2022 and to agree that such plans should include:

a. A minimum care need threshold to be eligible for subsidised care from the Long-term Care Insurance Fund;

b. Additional rates of benefit, lower than those that apply to care homes, to support people receiving care in their home;

c. A scheme whereby claimants receiving a subsidy towards residential or nursing care could in the future have the option of using this subsidy towards care in their own home

d. Criteria for establishing long-term need (for example care requirements likely to persist for at least six months or until end of life) which would qualify for a claim from the Long-term Care Insurance Fund; and

e. A suitable assessment process capable of establishing eligibility for benefit for those requiring care at home in a time and cost-efficient manner.

8. to agree that a reliance on increased contribution rates to ensure the financial sustainability of the Long-term Care Insurance Fund, in the context of the changing demography, risks an increasing and significant intergenerational unfairness.

9. To note that additional funding of up to £25million per annum, may be required; and

a. to direct the Policy & Resources Committee, as part of the Review of Taxation and in consultation with the ESS, to identify a suitable source of funding to ensure the long term stability of the Long-term Care Fund, in accordance with the principles of the Fiscal Framework; and

b. to direct the Committee for Employment & Social Security, if the Review of Taxation does not identify measures to ensure the long-term stability of the Long-term Care Fund, to propose within its annual contributory benefit report an increase in the social security contribution rate of a maximum of 1.3% with effect from January 2022.

10. To direct ESS, in co-operation with HSC, to continue to work towards establishing contractual arrangements with some or all care homes providers in order to provide certainty of income for the care home and certainty on the number of beds available at ‘States rates’.

Whilst the States have moved a step closer to providing for the costs of private care in peoples own homes there is as yet no agreement on how this will be funded which, at the moment is dependant on the Review of Taxation. This will need to be resolved this States term and will be a challenge for the new States.

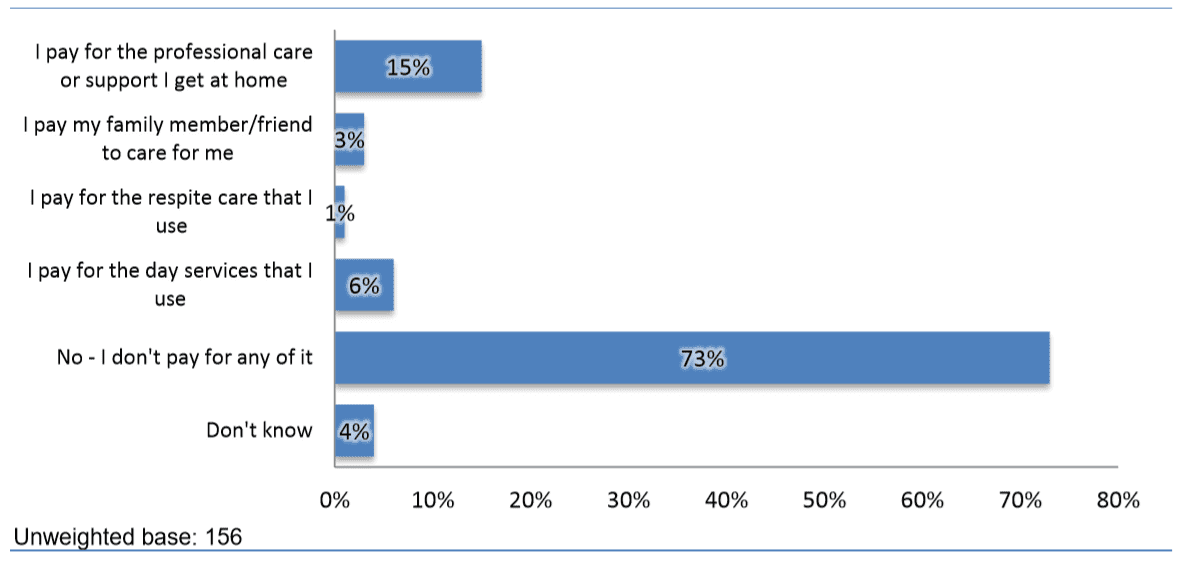

Figure. Can you tell me if you pay for any of the care or support you receive at the moment? (All valid responses – where receive care and support)

In 2012 research was undertaken in Guernsey that showed of the 156 respondents who receive care and support who responded, just 23% pay for this support. The majority (73% – 114 people) do not pay for their support and 4% say they don’t know. Older people with long term conditions are more likely to pay for their support (30% – 17 people aged 67+), especially the care that they receive in their home (20% – 10 people), as do 29% of people with a learning, understanding and development difficulty (16 people). 9% (4 people) of this latter group pay for the day services that they use.

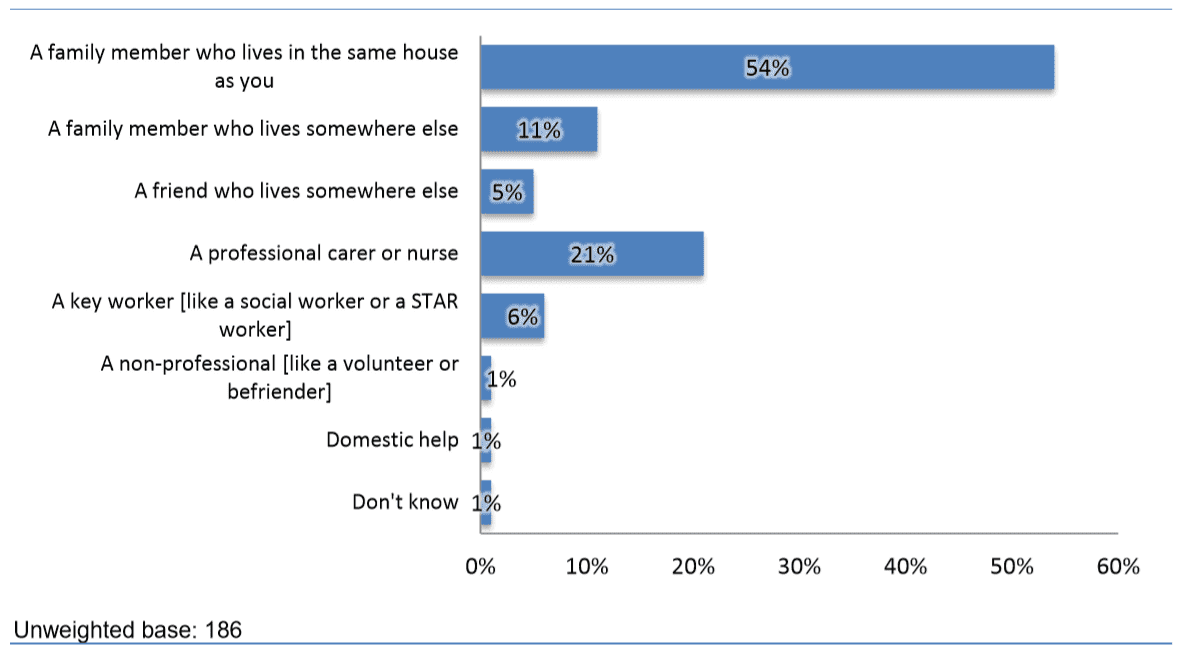

Figure. Can you tell me who you see as your main source of help and support? (All respondents – where receive care)

The 2012 research looked at many different aspects of life including, for those respondents with care requirements, who provides care and support. It is no surprise that the majority of respondents who receive care state their main source of care is a family member who lives in the same house as them (54% – 100 people). A further 1 in 5 (21%) regard their main source of support as a carer or nurse and 11% a family member that lives somewhere else. There are interesting variations by type of disability. Although support from a family member living in the same house is the most common form of support for all groupings, a professional carer or nurse is the main source of support for as high as 35% of respondents with “other chronic conditions” (20 people), 24% with mobility or dexterity problems (34 people), and 23% with sight or hearing problems (17 people). Respondents living in social housing are also more likely to regard a key worker as their main source of support (19% – 7 people), compared to just 3% of owner occupiers (4 people).

Supported Living and Ageing Well is an important policy for many of our members and we are conscious that with an ageing population more Islanders will require help and support to age well.